DeFi Business Models

New business models require new valuation frameworks

Hello readers,

And welcome to the 367 new subscribers that have joined our community over the last week. Crypto is in a bear market, but The DeFi Report continues to steadily grow. As always, our goal is to share our research of DeFi and web3 with you while breaking things down into easy-to-follow frameworks. We received a lot of fantastic feedback from our last report on tokenomics — in particular, folks responded well to the framework we provided for a web3 Uber network.

We’ve even had several entrepreneurs and founders reach out, and we encourage this. If you’re an engineer, developer, entrepreneur, operator, etc — please feel free to contact us directly if something we write sparks an idea — we’re always happy to chat.

This week we are diving deeper into DeFi business models. Topics covered:

How DeFi Protocols Grow and the Associated Costs

Total Revenue vs Protocol Revenue

Defining Profitability

Which Protocols are Profitable?

Projecting Growth and Value Accrual to the Token

If you’re new to The DeFi Report, drop your email below to receive free reports covering DeFi and web3 business models directly to your inbox.

Let’s go.

The Cost of Growth

How does a DeFi protocol grow? If we look at this from first principles, DeFi business models don’t look that different from traditional start-ups. As with any business, DeFi protocols have to “spend money to make money.”

How do they “spend money?”

They use their native token to incentivize the use of the protocol. That is, they give away tokens to users (demand) and service providers (supply) — those needed to bootstrap a multi-sided marketplace. The dollar value of these incentive programs is the “cost to grow.”

This is akin to a start-up focusing on growth, allowing their expenses to far exceed their revenues in order to lock in users and create a network effect. VCs and early investors essentially foot the bill for this. Every tech platform we use today started this way.

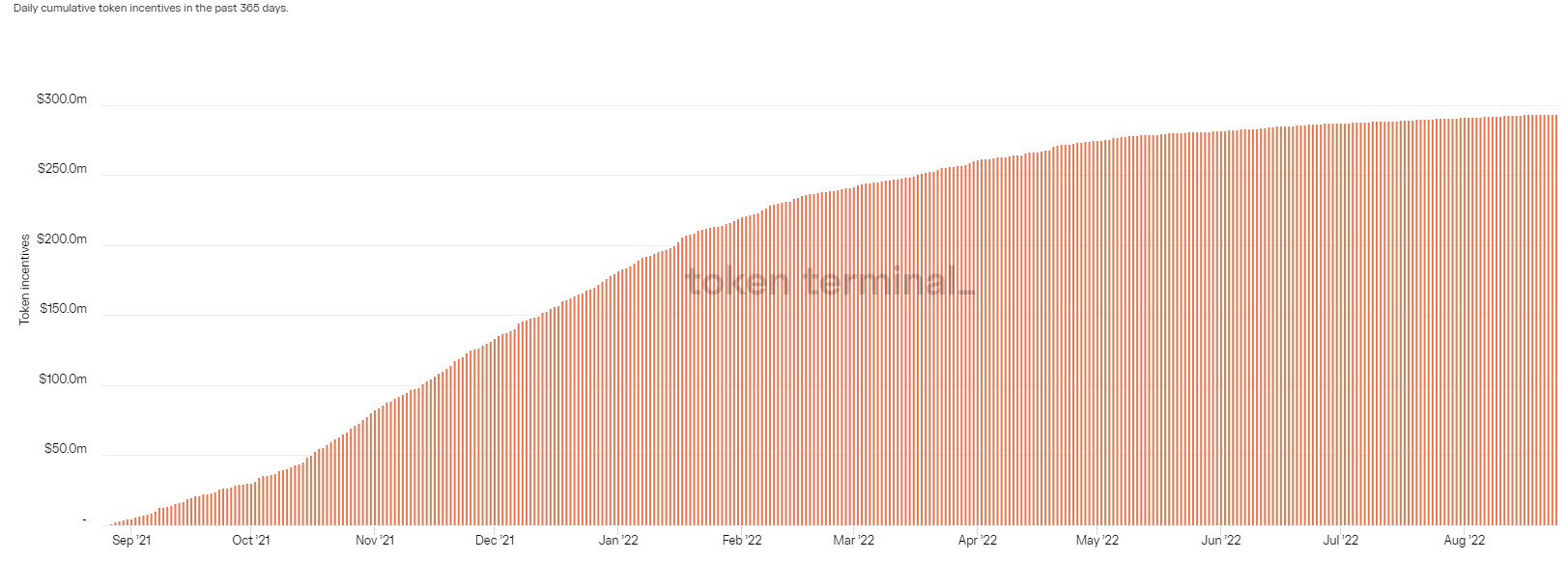

Here is a view of Uniswap’s “token incentives” since the protocol launched.

Data: Token Terminal

Shortly after Uniswap made some major product updates and launched v2, they distributed tokens to users and service providers (liquidity providers in the Uniswap ecosystem) — $66 million worth. These are the same tokens that a16z, one of the most powerful VC firms in the world got when they invested in Uniswap.

Let that sink in for a second — this is the power of tokens and why they can be an incredible tool for bootstrapping *open internet services.* Of course, the incentives have to work and users and service providers have to stay for the long run. In the case of Uniswap, they have to keep their liquidity providers happy. So far so good on this front.

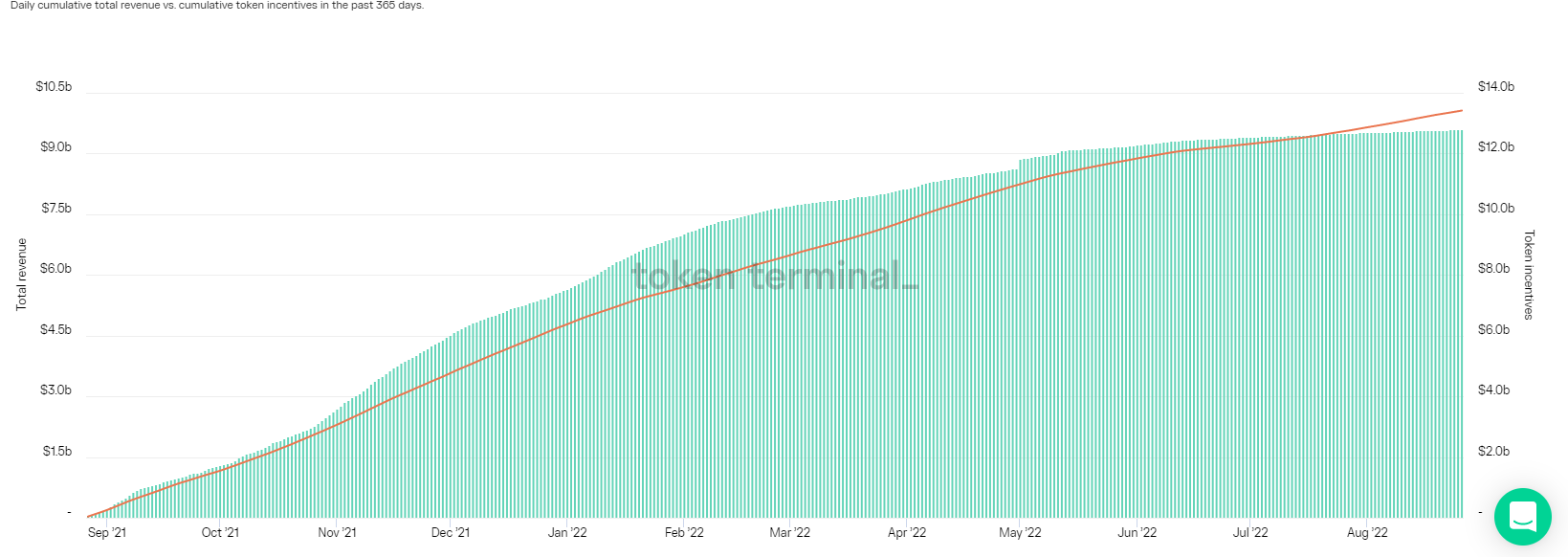

Meanwhile, here is what happened with revenues on Uniswap since those incentive programs:

That’s $2.4 billion paid to the folks they incentivized to join the network. No wonder Uniswap has been able to hold a 70% market share amongst AMMs, even though their code can be copied/forked at will.

Later, in early 2021, the Uniswap DAO voted to incentivize the adoption of Uniswap on Arbitrum and Optimism, two Layer 2 scaling solutions built “on top” of Ethereum. If you’re interested in reading the DAO governance proposal and discussion amongst the community - check it out here. Note that the proposal took 3+ months to go through, which highlights issues with DAO governance and decision-making in its current state — a topic for a future report.

Key Takeaway: DeFi networks use their token to incentivize the formation of two-sided markets (supply and demand) to build out the usage of their products/services. This is just a better tool with less friction and more scalability than strictly using VC dollars. And just like a network like Uber (funded by VC dollars) had to eventually stop with the freebies/incentives and make real money, DeFi protocols have to do the same.

Total Revenue vs Protocol Revenue

Here’s Uniswap’s total revenue over the last 365 days.

$1.2 billion — paid out 100% to liquidity providers. This is akin to Uber paying their drivers 100% of the ride fares. This is by design. It is critical for Uniswap to build out a sticky network effect in its early years. Liquidity providers are essential to this process.

That said, there has been a stir recently regarding when Uniswap would turn on the “fee switch.” The DAO recently approved a pilot program where a 10% fee will be returned to the protocol treasury from 3 pools for a period of 4 months. The idea is to gauge how this impacts their LPs, overall liquidity, total revenues generated, etc. Various DeFi protocols, such as Aaave (lend/borrow app) currently take 10% of the total revenues generated. We can see this below — total revenues over the last year shook out to $315m (light green) for Aave, while the DAO treasury retained $31.5m (dark green) as their protocol revenues.

But what did Aave have to “pay” in token incentives to generate those revenues?

About $290 million.

It may look like Aave is overspending for growth right now, but they also have the 3rd most total value locked in DeFi and did about 10x the revenue of its closest competitor. So far, they are getting what they paid for. But again, at some point, these incentives have to end. And the users and service providers have to stay.

Defining Profitability

This is open for debate right now because these are entirely new business models. The truth is, nobody actually knows how to define profitability yet. Or how to value these networks as we do not have a standard just yet. There are a few questions we have to ask ourselves to get started:

First, should we think of profitability as total revenues - token emissions? In this context, we would define token emissions as the tokens distributed to the users needed to bootstrap an ecosystem — i.e. supply (service providers) and demand (users) — not including investors and the team. We define total revenues as the amounts paid directly to service providers + revenues paid back to the protocol (if any).

From the Layer 1 perspective:

Total revenues for Ethereum = total transaction fees paid to miners/stakers. Similar to Uniswap, Ethereum has no “protocol revenue.” 100% is paid to its service providers.

Total revenue (green) = $9.6 billion. This includes transaction fees only. Total expense = $13.4 billion. This is the block subsidy paid to the miners. But is this the right way to think about it? Or should we think of the expenses as simply the cost of mining (energy cost + machine cost) or staking (the up-front cost of the coins staked)?

The bottom line is that for a Layer 1 blockchain to maintain long-term viability, its service providers (miners or stakers/validators) need to be profitable. This is the case today for Ethereum and Bitcoin. In each case, as the block subsidies drop (as is happening with Ethereum via the merge and with Bitcoins halving schedule), the transactions must ramp up to offset the decrease in block subsidies to compensate service providers. No service providers = no network.

From the DeFi application perspective:

The same is true for DeFi applications. The bottom line is the service providers need to be incented to stay in the network. For Uniswap, this is the liquidity provider. These folks earned $1.2b in fees last year. Their expense is the cost to acquire that liquidity.

The protocol’s expense is the cost to incentivize the liquidity providers to join — by giving away the token. And the protocol’s revenue is their % take of the revenue made by the service providers — 0% in the case of Uniswap today, though as mentioned, they are currently running a pilot program to claw back 10% from 3 select liquidity pools.

See how this gets confusing?

There are a few critical elements going on here.

The network has to properly compensate its service providers. For layer 1’s this is the miners or validators. This allows for the formation of a network effect, and a further compounding network with the usage of the blockchain or app/protocol.

These incentives allow the network effect to take hold. If successful, the number of people using the network allows for transaction fees or service fees to take over and the incentives or subsidies are no longer needed to maintain the network.

If a massive network is formed, eventually the token holders can direct a portion of the total revenues back to the treasury or directly to the token holders.

Therefore, our take is that in the early days, a network’s profitability comes down to the total revenues (protocol + payments to service providers) less its token emissions. And we don’t care about profitability in the early years.

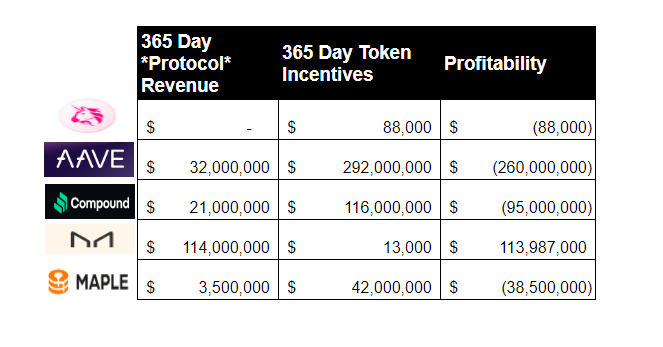

Using this definition for profitability, here is a quick view of what some of the DeFi blue chips look like today:

But what if we only look at *protocol* revenues — the funds that are currently re-directed from the service providers back to the protocol treasury? This paints a different picture:

MakerDAO starts to stand out all of the sudden — because MakerDAO has basically zero token emissions (unless they need to mint new MKR tokens during a period of extreme volatility). MakerDAO does not have decentralized “service providers” as well — therefore 100% of revenues are captured by the treasury. If you’re interested, we wrote about MakerDAO last year.

Of course, there is further nuance to explore here. The Uniswap Labs team (those working on the protocol) are not receiving any of this revenue. But they have expenses. Like an office and payroll — just like any other company. They pay for this with the $ VCs seeded them with and also with funds from the DAO treasury if needed. MakerDAO has almost zero token incentives, but they have about 100 employees or “core unit” members. Here is how profitable MakerDAO is when we factor in the “core unit” expenses — DAO payroll and operating expenses.

Source: MakerDAO July 2022 Financial Reports https://drive.google.com/file/d/17VlihhTaeE40EKvbXrWQ-NASa6p9lc2k/view

MakerDAO made $80 million in profit over the last year — most of which during a bear market.

Value Accrual to the Token

This is the tricky part.

Ponder this: imagine if Google paid out 90% of its advertising revenue to users of Google. And 10% went to the core developers and engineers to make the network function properly. Let’s assume Google’s service offering is the same as it is today under this new model. The same # of people use Google.

Is the network worth more or less with this new business model?

And if you own the right to how Google’s revenues are directed in the future (via a token), how do you value that right?

This is the challenge we have today with valuing crypto tokens. If it’s obvious that a network has value based on its usage, utility, revenues, etc and the token represents a right to direct where those revenues accrue in the future, how do we value the token?

We have to throw out the old methods that we use to value companies.

But we can come up with frameworks for proxies to value: Addresses (proxy for users), Price to Sales, Total Value Locked, Total Revenues, Liquid Treasury balances, etc.

*A significant portion of liquid treasuries is sometimes comprised of the native asset of the protocol. For details on what makes up the treasury, go to openorgs.info.

Summary

DeFi protocols “spend money” with the native token of their protocols — to incentivize the formation of multi-sided networks for open internet services.

Some protocols are currently directing a % of the service provider revenues back to the protocol treasury for future growth. Others continue to build out a network effect by allowing the service providers to capture 100% of the service revenues.

Profitability can be measured in terms of Total Revenues less Token Emissions or Protocol Revenues less Token Emissions. Keep in mind that although a network like Uniswap does not have protocol revenues today, they could “turn the fee switch” on in the future — something the Uniswap DAO is currently experimenting with.

Valuing tokens today comes down to analyzing the network effects of these protocols using the available data. However, since revenues do not accrue directly to tokens today, it is very difficult to assess value. That said, it is not uncommon to assign value to traditional companies that do not pay dividends in the early phase of growth (as all DeFi projects are in today).

If you can envision a future where dividends accrue to token holders, it will be much, much easier to value these tokens using traditional methods such as discount cash flows. And the market will suddenly “get” these new business models and price them as such.

I hope this helps provide some clarity into DeFi business models, DAOs, and how the token can help bootstrap the early days of growth.

___

Thanks for reading and for your continued support. If you got some value from this week’s report, please like this post, and share it with your friends, family, and social networks so that more people can responsibly learn about DeFi and web3.

It costs nothing for you and will make my day!

If you have a question, comment, or thought, please leave it here:

If you are interested in any kind of partnership, sponsorship, or bespoke consulting services feel free to reach out at mike@thedefireport.io or reply to the email if you are reading this from your inbox.

___

Take a report.

And stay curious my friends.

Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional and may hold positions in the assets covered. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general educational purposes only, is not individualized, and as such does not constitute investment advice.