MakerDAO

Is MakerDAO an emerging (De) Central Bank?

Hello readers,

I hope everyone had a nice weekend. Buckle up, this week we are going deep on the OG DeFi application, MakerDAO. MakerDAO is arguably the only truly decentralized DAO in crypto today. It is by far the most successful DAO and has the longest track record to analyze.

I have been particularly interested in MakerDAO’s recent move into lending on real-world assets. A few weeks back, Tesla quietly used MakerDAO to finance the build-out of real estate investments in the US (collision centers). Tesla is the 6th largest company in the world by market cap. They didn’t use JP Morgan, BoA, or Wells Fargo for these financing deals. They used a DAO built on Ethereum. Let that sink in for a minute.

While somewhat under the radar, MakerDAO has been quietly building an extremely robust and battle-tested lending/borrowing application while growing its native overcollateralized stablecoin, DAI. The DAO’s stablecoin functionality, governance, risk aversion, and overall importance to DeFi make it one of the most important projects in crypto.

In this report, we’ll cover everything you need to know about MakerDAO.

Topics covered:

DAO Basics

The Functionality & Importance of DAI - the overcollateralized stablecoin powering the MakerDAO ecosystem

DAI & Lending on Real-World Assets

MakerDAO’s Functionality as a Crypto (de) Central Bank

The Maker Token Economics & Incentive Structure

Is MakerDAO Good or Bad for the Dollar?

As a reminder, if you’re new to the program, you can drop your email below to receive these free reports directly into your inbox as they are published.

Let’s go.

DAO Basics

DAO stands for decentralized autonomous organization. The idea here is that a group of people can come together with a shared vision and execute that vision in a more decentralized manner by leveraging blockchain technology and smart contracts. We can think of this similar to how we think of crowd-funding. A group of people comes together with a shared goal. They contribute money to buy tokens which allows them to vote on key decisions that are critical toward reaching the shared goal - through which all members benefit. The difference from traditional crowdfunding is that there is no central authority making decisions in a DAO structure. The rules of the DAO are coded into smart contracts, which execute autonomously. Hence, the name: Decentralized Autonomous Organization.

If a DAO can get its governance right, everyone participating gets to share in the upside. This is what is so exciting about DAOs. They are potentially a paradigm shift for corporate structures. Typical corporate structures have founders and investors (to some extent, early employees) that participate in the upside of the company. Users or customers can also be investors, but there is no direct linkage. In a DAO, the lines are blurred. The user is more often the equity/token holder. Token holders are like board members - steering the company by voting on key decisions. This same person could also work for the DAO. By decentralizing governance and establishing a level hierarchy, DAOs seek to spread the benefits and upside more evenly across users/employees/investors, and the general community. With a properly governed DAO, you get shareholder alignment. Aligned incentives. To date, the best use case for DAOs has been in DeFi.

MakerDAO

MakerDAO has 5 core features:

Decentralized Bank - anyone with sufficient collateral can mint DAI and get a loan (no credit or income checks required)

Savings Account - anyone can deposit DAI, Maker’s overcollateralized stablecoin, to earn a yield in excess of the yield offered by traditional banks

Generates DAI - an overcollateralized stablecoin soft pegged to the dollar that can be used for loans, payments, and remittances. Interest paid on DAI loans funds the DAO.

Loans on Real-World Assets - MakerDAO is the first DeFi application to interact with real-world financing deals

Decentralized Central Bank - MakerDAO feeds liquidity into the rest of the DeFi ecosystem.

There is a LOT to cover here. Grab yourself a coffee, tea, or an adult libation if that suits your fancy. Pro-tip: read this one slowly, stopping and thinking along the way.

MakerDAO was formed in 2014 and officially launched its Stablecoin, DAI, on the Ethereum mainnet on December 18, 2017.

The stated goal of MakerDAO is to create a decentralized, transparent, and accessible platform to level the economic playing field for everybody around the world.

DAI

Dai is the overcollateralized stablecoin that is soft-pegged to the US dollar. It is undoubtedly the most important feature of the MakerDAO protocol. DAI is minted when users seeking loans deposit collateral (Bitcoin, Ethereum, etc) into vaults within the protocol. Connect your wallet and deposit $100 worth of BTC or ETH into a vault, and you can mint about $66 work of DAI. Congrats, you just received banking services with the click of a mouse. The loan is overcollateralized lending. This is due to the volatile nature of the cryptoassets used as collateral. Liquidation of a user’s collateral occurs when its value drops below the amount of the DAI issued.

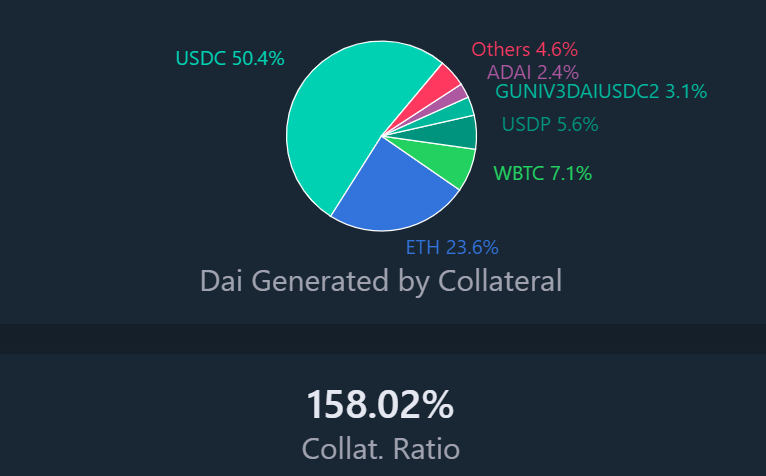

Here is a quick view of the assets backing the DAI in circulation today.

You are probably wondering why there is so much USDC backing DAI. Why would a centralized stablecoin back a decentralized one?

Anyone can mint DAI 1:1 against USDC with zero interest due on the DAI. This means that if the price of DAI goes above $1, anyone can go swap dollars for USDC, trade it for DAI, and then sell the DAI, taking the spread as profit. This forces the peg of DAI back down to a 1:1 ratio with the dollar. A similar trade can be executed if DAI drops below the dollar. This is incredibly useful for the protocol as it reinforces DAI’s peg to the dollar. So, the DAO is accumulating a ton of USCD on its balance sheet. This is deep liquidity for DAI against dollars which serves as a capital battery to supercharge real-world asset lending or investment in safe, extremely liquid assets like US treasuries. The DAO basically has $5 billion on its balance sheet that it can use to earn a yield/revenue for the DAO.

Here is the total supply of circulating DAI over time:

Source: Makerburn.com

And here is a breakdown of where DAI is locked within the crypto ecosystem:

Source: Makerburn.com

DAI is paid back to the protocol with interest (currently 2.25%). This is what funds the DAO. 2.25% on $9 billion of outstanding DAI equates to annual revenue of over $200 million. These revenues pay for the core units - the folks who work for the DAO. This includes engineering teams, oracle teams, ops teams, governance teams, finance teams, risk teams, etc. The interest (stability fees) paid back also helps to maintain the peg to the dollar (adjusting it changes the supply of DAI), and burns the Maker token (the governance token/the token you buy to invest in MakerDAO). Finally, portions of the interest/stability fee go toward the Surplus Buffer. This is the excess DAI that is held in reserve for bad loans and currently sits at $69.5 million. If a borrower defaults and the protocol has bad debt, they use the surplus buffer to pay it off and everything is all good. As the surplus buffer grows, MakerDAO can increase its tolerance for individual defaults. This risk is spread across many protocols and borrowers such that there is independent risk in each area. Does this sort of sound like traditional finance? This is very much how traditional bank lending works - losses and bad debts are expected and planned for. It’s all about risk management.

So, what exactly does all of this mean?

It means that the #1 goal of MakerDAO is to grow the supply of DAI. This is what funds the DAO, drives the value of the Maker token, and adds to the Surplus Buffer - which allows the DAO to expand DAI lending on additional protocols, to lend on real-world assets, expand reputation-based lending, expand undercollateralized loans, better manage risk, etc.

What drives demand for DAI?

MakerDAO is functioning similarly to a bank, except it is decentralized. When people are willing to hold DAI, they are lending MakerDAO money, which is lent out to those using the vaults to borrow money. The interest paid back funds the DAO. The principal paid back is burned (just like principal paid back to traditional banks reduces the money supply).

Let’s say you own a bunch of ETH or BTC and you want to buy a house. You may not want to sell those assets and incur a tax liability. So, instead, you lock them up in MakerDAO, take a loan of DAI at 2.25%, and purchase your home (convert DAI to USD), while still capturing the upside of your crypto holdings, and avoiding a taxable event.

Crypto traders also leverage the protocol by locking up collateral for loans to trade assets and enhance their yields.

We are now starting to see demand from corporates for DAI since the DAO is able to undercut rates offered by traditional banks. Due to the liquidity of DAI, Corporates (like Tesla) can easily swap their DAI for dollars (for commercial interests), and later pay the back the loan in DAI.

Finally, lending/borrowing apps that sit above MakerDAO in the DeFi tech stack leverage access to DAI to control interest rates during periods of extreme demand for loans. As interest rates spike on these protocols, they can mint DAI to add liquidity and bring rates down to more reasonable levels, which protects their borrowers and secures the system. I’ll cover this more in a later section.

How does DAI Maintain its Peg to the Dollar?

As mentioned above, the $5 billion USDC acts as a peg for DAI to the dollar for arbitragers. There is no interest or over-collateralization requirements for depositors of USDC. The DAO earns nothing on USDC (unlike BTC, ETH, or Real World asset-backed loans). However, they are ok with this because arbitragers use USDC to earn spreads which in turn maintains the peg. And MakerDAO then uses the USDC on its balance sheet to invest in a bevy of low and higher-risk areas to earn revenue for the protocol.

Maker token holders also vote on the interest rate/stability fee which changes the supply of DAI and helps to manage the dollar peg.

DAI & Real-World Asset Lending

The goal is to expand the supply of DAI and create utility in the real world. This takes us into MakerDAO’s plans for lending on real-world assets. MakerDAO grows as a protocol (and the Maker token appreciates in value) when they grow the supply of DAI. It’s all about growing DAI and they are taking a very slow, thoughtful, risk-averse approach to do so.

Lending on real-world assets is a very different model than overcollateralized crypto loans. It’s much more complex (there are third-party credit facilities like 6s Capital and Maple Finance involved as well as a number of legal entities). All of the interaction is not on-chain today (such as the legal entity holding the collateral that the DAO has a claim to). The DAO considers these loans riskier than overcollateralized crypto-backed loans. Therefore, the DAI Supply Buffer has to reach certain thresholds before MakerDAO initiates loans on real-world assets. This has officially commenced, as Tesla recently financed real estate collision centers in the US with a $7.8 million dollar loan in DAI. The loan is backed by the real estate itself. This is pretty wild to think of. Most people never thought DeFi would get to this stage - providing real value and utility to the real world. I’m hearing that Tesla and MakerDAO have very big plans and that the first loan was just the tip of the iceberg.

It should be noted that the DAO is very mission-focused. Ultimately, the Maker token holders decide (through governance voting) which loans can be approved, but there is a clear focus today on green energy projects.

Is MakerDAO a Decentralized Central Bank?

Anyone can mint money on MakerDAO by depositing collateral into a vault. So, yes, this is definitely a decentralized bank. It is also showing signs of acting as a Central Bank.

The Fed adds and removes liquidity in the traditional banking system by increasing/decreasing interest rates by purchasing (or not purchasing) treasury bonds. When they do QE, they are monetizing the treasury’s debt by printing money and then swapping it for bonds with the commercial banks. The commercial banks then lend off of these bank reserves which ultimately adds liquidity to the market.

MakerDAO is functioning in a similar manner within DeFi (except they don’t do QE). They set interest rates that add to and reduce the liquidity of DAI in the market. They also provide liquidity to Aave and Compound (decentralized lending/borrowing apps) that cannot print their own money. For example, when rates spike on these platforms, borrowers get squeezed. This is not good for the users or the system at large. When this happens, these protocols get liquidity from MakerDAO which pushes interest rates down and maintains stability in the system. This is pretty similar to how the Fed interacts with the commercial banks (JP Morgan, BoA, Wells Fargo, etc) in traditional finance.

Source: https://hexonaut.medium.com/maker-past-present-and-future-9fd67da4f229

Historically, the Fed has not had any competition. They have a monopoly on the creation of money. MakerDAO appears to be new competition for the Fed as it is the only other entity that can print (collateralized) money that I can think of. Pretty interesting.

Maker Token

Maker is the token you buy if you want to invest in MakerDAO. If you believe that the DAO can manage risk, expand DAI, and earn more and more revenue over time, buying the token is a way to express your thesis.

If you own the Maker token, you also get to vote on key decisions of the DAO such as interest rates, collateral to be added, new protocols to add DAI liquidity to, real-world asset loan approvals, etc.

Supply of Maker

This is critical in understanding how value accrues to the token. Maker was released into the market with 1,000,000 tokens. There are currently 977,631 tokens on the market. The supply of Maker drops as a portion of the interest paid on DAI loans goes toward burning the Maker token. Maker supply also drops when borrowers are liquidated as the collateral goes to auction where users can bid on the collateral (at a discount) in Maker. The winner of the auction receives DAI and the Maker is burned.

Maker supply increases during volatile periods where the total collateral backing DAI is lower than the amount of DAI circulating. This happened in March of 2020 when global markets rapidly sold off. To re-collateralize DAI, the protocol had to mint new Maker tokens which are auctioned for DAI, recapitalizing the system. This is dilutive to holders of the Maker token and is designed to create proper incentives for managing risk within the protocol.

It is worth mentioning that the DAO has never focused on the Maker token. You will almost never hear it mentioned. The focus is on managing the protocol and growing the supply of DAI. If they do this well, the Maker token will see price appreciation over time.

Is MakerDAO Good or Bad for the Dollar?

This is a fascinating question. My take on this is that in the short term the DAO is actually good for the dollar. In the long term, maybe not so much.

Let me explain.

Over half of the collateral backing DAI today is USDC. USDC is a regulated stablecoin that is fully backed by dollars and short-term treasury bonds. USDC has a total market today of over $50 billion (10% is locked in MakerDAO). Dollar-backed stablecoins are a source of demand for dollars globally. This reinforces the network effect of the dollar around the world. You don’t see any stablecoins backed by Euros, Chinese Renminbi, or Japanese Yen.

Furthermore, DAI is not a unit of account or medium of exchange outside of crypto. So, any corporate entity receiving loans in DAI is swapping them for dollars for their commercial/business interests, and then swapping back to DAI to pay the principal and interest. This action is neutral for the dollar.

It is important to note that the dollar is what is fueling crypto today. The collateral backing DAI (BTC, ETH, etc) uses the dollar as its unit of account. So, as the Fed prints money and adds excess liquidity into the economy, some of this is making its way into crypto. As more dollars flood into BTC and ETH, more collateral is posted to MakerDAO, and more DAI is minted. As more DAI is minted, DAI liquidity increases. More people start using DAI. If DAI’s supply and utility as a unit of account/medium of exchange rapidly increase, there could potentially be less need for the dollar at some point.

My base case here is that DAI supply (and crypto at large) will continue to grow. But the dollar will not go anywhere - the two will co-exist. Over time, we will simply see competing alternatives to the dollar (in addition to many, many more use cases) and fiat currencies in ways that we have not seen in recent history. As mentioned, the dollar is fueling crypto. And in many ways, crypto is actually enhancing the dollar’s network effect (via stablecoins backed by USD & Treasuries).

In the very, very long run, it is certainly possible that the dollar self implodes. It is reasonable to anticipate this could happen, especially in light of the balance sheet of the United States and current geopolitics. Every fiat currency in existence has died throughout history. I see no reason to believe the US dollar will be different in the long run.

If this were to happen, Bitcoin (and possibly ETH) could become a base layer monetary asset as Gold was throughout history. Fiat currencies or stablecoins like DAI could be pegged to these assets as part of a new, global monetary system for the internet. Nobody can predict the future, but if this were to occur, it would likely be 10+ years out. The ideal scenario for crypto (and society) I believe would be for crypto to serve as a slow, drawn-out off-ramp for the dollar. If fiat currencies were to de-stabilize at a more rapid pace, it’s possible that governments would try to enforce capital controls in an attempt to stop the spread of crypto.

Risks

As with many businesses in crypto, MakerDAO is completely dependent on BTC, ETH, and other cryptoassets growing in value. More BTC and ETH value equals more collateral. More collateral equals more DAI. More DAI equals more revenue for MakerDAO.

Additional risks include flash crashes (black swans such as March 2020), challenges with protocol governance, smart contract/oracle hacks, and competition from other stablecoin networks such as Terra.

___

Thanks for hanging with me for this extra-long version of The DeFi Report. MakerDAO is a complex protocol, but anyone that devotes the time to study it will find that it is very well run (risk-averse), has proper incentive structures, and plays a critical role within DeFi.

If you got some value from this week’s report, please share it with your friends, family, and social networks.

If you have a question, comment, or thought, please leave it here:

Looking for a job in crypto? Check out the list of openings with The Crypto Recruiters here.

Finally, if you would like to send me a tip, you can do so through the addresses below. If you do send a tip, please be sure to let me know so that I can send you a thank you note.

___

Take a report.

And stay curious my friends.

Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general investment information only, is not individualized, and as such does not constitute investment advice.