What the heck is going on out there?

Bank Runs, Bitcoin, and the Crypto Crackdown

Hello readers,

I’ve been thinking a lot lately. Like, a lot. It’s dangerous, I know. There are so many things happening in the markets right now, it is difficult to keep up. Exciting stuff. Scary stuff. And lots of unknowns. This report is a summary of the “big picture” stuff going on as I see it, and where we go from here. Topics covered:

State of the Banking Sector

Bitcoin

The Ongoing “Crypto Crackdown”

What’s next? Incoming QE.

Disclaimer: Views expressed are the author's personal views and should not be taken as investment advice. The author is not a registered investment advisor.

The DeFi Report is an exploration of the emerging web3 tech stack and an ongoing analysis of where value could accrue. We provide data-driven analyses of DeFi and web3 business models.

We also occasionally delve into macro-focused reports, such as this one.

Let’s go.

The State of the Banking Sector

I’m sure everyone is aware of the fall of Silvergate, Silicon Valley Bank, Signature Bank, and Credit Suisse (acquired by UBS) by now. And we continue to hear rumors that additional large regional banks such as First Republic and PacWest are on the ropes. Many smaller regional banks could be under similar distress, but we do not know which ones — because usage of the Fed’s new BTFP program is shielded from the general public. And now we are seeing similar warning signals emanating from abroad.

How did we get here?

In my view, the issue can be summed up quite simply: banks purchased a bunch of treasury bonds at near-zero interest rates — which allowed the government to fund fiscal spending throughout Covid. But then inflation reared its ugly head. And the Fed was forced to raise interest rates at the sharpest pace in recent history. The banks were caught off guard because inflation was supposed to be “transitory.” So, now the banks are holding these assets at significant discounts (rising rates = lower bond prices). Meanwhile, interest rates are near 4.5% for money market funds — incentivizing depositors to move their money. Banks aren’t paying anywhere near that rate. Because they can’t. The business model of banking does not work when the yield curve is inverted for an extended period. It’s been inverted now for a year.

So we have a perfect set-up for bank runs. Hence the Fed and Treasury stepped in with the Bank Term Funding Program — which allows the banks to collateralize discounted assets at par for loans up to 1 year. This bolsters the bank’s capital reserves and helps to calm market psychology and fear.

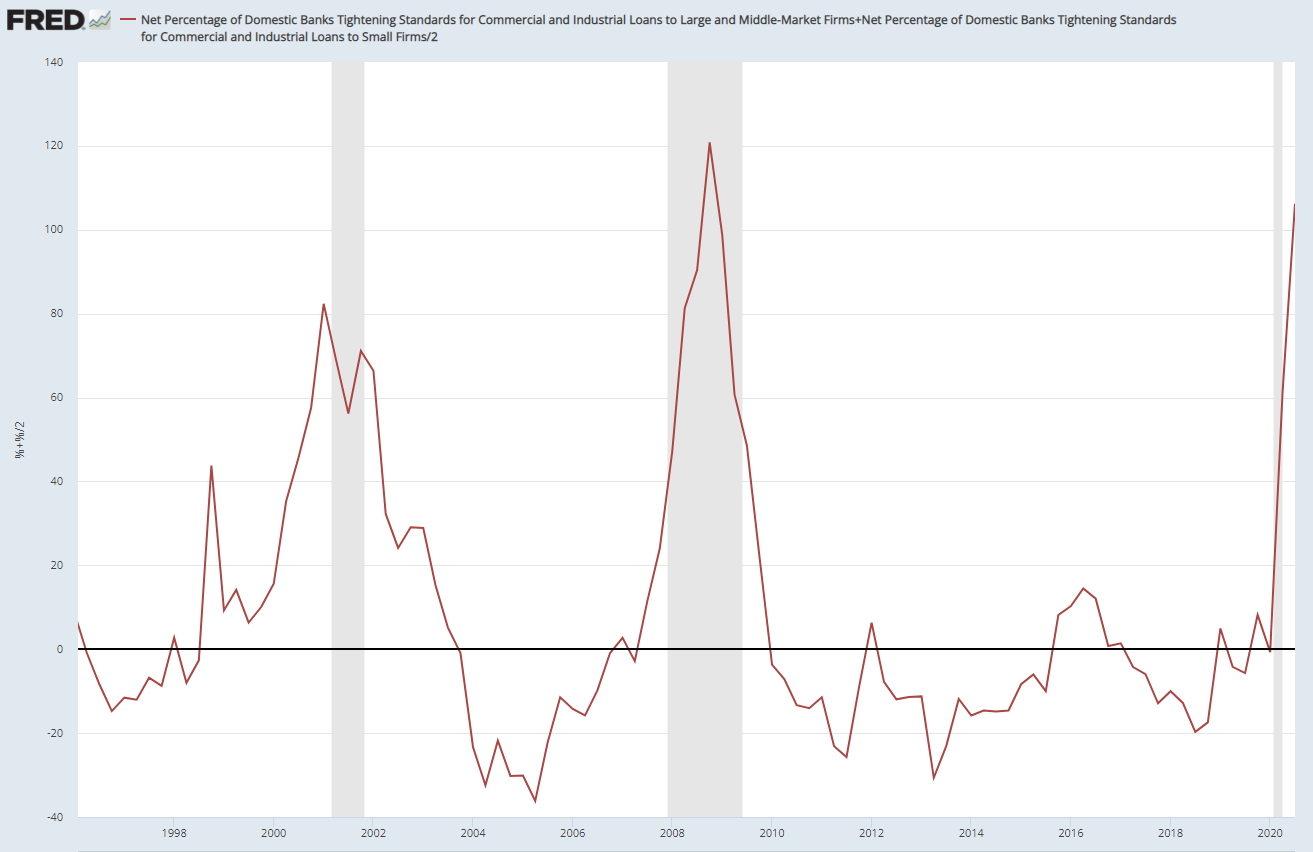

However, the crisis is not yet averted. Banks still aren’t lending.

In a credit-based system, a lack of credit leads to dollar shortages. Which eventually leads to the selling of assets. And so, the Fed as the lender of last resort (via newly created money) is stepping in once again.

Is this QE?

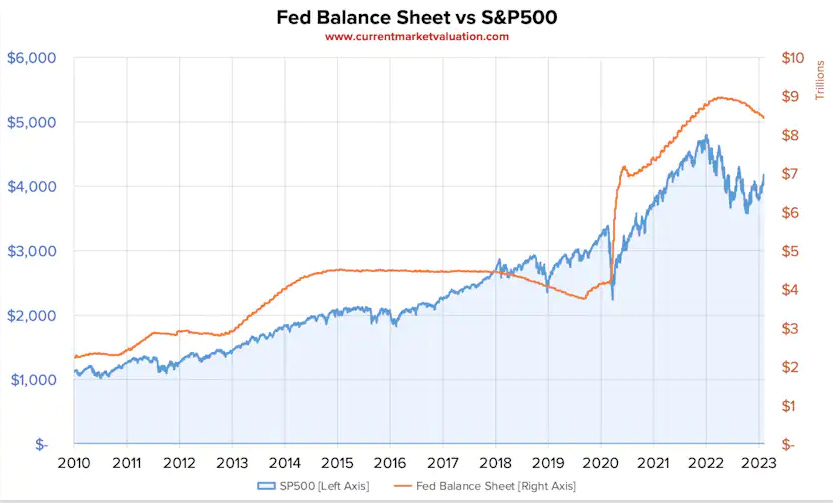

I continue to see this debate over whether the BTFP program is “QE” or not. It’s a silly debate over semantics in my opinion. The mechanics of BTFP are different from QE. But the effect on the Fed’s balance sheet has been the same: it’s going up!

This is all we care about. Because the Fed’s balance sheet is tightly correlated to the performance of the S&P 500. We’ll come back to this later in the report when we get to where this is all heading.

More Bank Runs?

I don’t have a strong take or any good data on this. The Treasury and Fed are now indicating that they will bail out smaller regional banks if needed. It seems clear that the Fed will have to backstop the entire system once again to instill confidence.

But what about the rest of the world?

The Eurodollar Market (US dollars outside the US, and not counted in M2) is estimated to be nearly as large as the US dollar market, which is currently $21 trillion. So, there could be just as much dollar debt abroad. But the ECB cannot print dollars.

And we continue to see signs of stress overseas. Credit Suisse (Switzerland’s second-largest bank) just went down and was acquired by UBS. Now Deutsche Bank (Germany’s largest bank) is showing signs of weakness. Who’s next? And who is going to be the lender of last resort?

We don’t know the answer to the first question. We do know the answer to the second question — the Fed. The Fed has to bail the entire global system out again. And it’s already starting to happen:

Unfortunately, the Fed did not release which Central Bank borrowed the $60b of funds.

But I think we can see where this is heading. We have a shortage of dollars. Which is due to monetary policy. And it’s a problem. The solution will also be monetary policy. Or more QE.

Final Note on the Banking Sector and Bank Runs

Perhaps the most important takeaway regarding recent bank runs is that money is moving FAST out there. The combination of social media and online/mobile banking systems makes it such that bank runs can occur within a matter of hours. It’s truly stunning. As I watched this play out, I immediately thought about the whole “meme stock” saga in January of 2021 — when a Reddit chat group took down a large hedge fund via a short squeeze of Gamestop shares. The powerful nature of online communities as it relates to financial markets and the “big, hot ball of money” moving around out there is the story to pay attention to in my opinion. It’s concerning that regulators are unlikely to be prepared for what could happen in a true crisis.

Remember, Bitcoin is just an “online community.” But it has hundreds of millions of users.

Let’s talk about that. Is Bitcoin about to have the moment everyone has been waiting for?

Bitcoin

Balaji Srinivasan, author of The Network State, Venture Capitalist, and former CTO of Coinbase recently made a very public bet that Bitcoin will rise to over $1m/BTC in the next 90 days as the banking system collapses and the Fed prints helicopter money.

This is highly unlikely in our view. And if something like this did happen (or begin to happen), we would expect to see capital controls in one form or another. Anyways, it’s an interesting bet from Balaji. A nice marketing campaign for Bitcoin if nothing else. I will say, it’s a fascinating (and scary) thought experiment to imagine a world where the banking system fails, the government prints helicopter money, and it flows into crypto and other hard assets. Again, unlikely. But if this did somehow happen, we would have to find a way to distribute Bitcoin and other crypto assets. We would have to integrate it with global merchants at the point of sale. Finally, we would have to make it a unit of account to reset global pricing to BTC decimals. A messy process. However, if this did start to play out, the open-source nature of Bitcoin (and crypto) could catalyze a rush of innovation to fill the market needs. Highly unlikely, yet not completely out of the realm of possibility.

Back to reality. We think Bitcoin is well-positioned to do very well as the liquidity cycle shifts. But keep in mind that in the very near term, we may actually see the price drop. In our opinion, we need to see a true liquidity event, and a clear signal from the Fed that we are going back to QE and low-interest rates before Bitcoin ultimately surges to new highs. We are seeing strong signals that this is coming, which we’ll get to later in the report.

The Crypto Crackdown

Now. I can’t even believe I have to write this next section. But here we are. The tin foil hat is on.

I’ve been shocked to observe what appears to be a coordinated shadow ban on crypto in the United States over the last few months.

Below is a timeline of what we’ve observed:

On Dec. 6th, Senators Elizabeth Warren, John Kennedy, and Roger Marshall sent a letter to crypto-friendly bank Silvergate, scolding them for providing banking services to FTX and Alameda Research. Mind you, Silvergate was burned by FTX and Alameda just like everyone else.

On Dec. 7th, Signature Bank announced its intent to cut its crypto deposits in half. This would reduce exposure down to $10b from $23b. They would also exit their stablecoin business. Signature bank was later shut down on a Sunday, March 12th. Details are opaque and unclear. Barney Frank (Signature Board) claims the bank was solvent. The FDIC later forced the buyer of Signature Bank to retire the crypto business, which included The Signet, a 24/7 digital payments liquidity market that met the needs of crypto companies and exchanges that deal in global, 24/7 markets. This is critical infrastructure providing liquidity for crypto markets. It’s now gone as Silvergate had a similar network.

I won’t add much more here, but if you want to learn more about the bizarre Signature Bank situation, check out this interview with Caitlin Long (CEO of Custodia Bank) here. The 47-minute mark is where the Signature discussion starts.

Moving on…

On January 3rd, 2023, the FDIC, OCC, and Fed issued a joint statement regarding “Crypto Asset Risk to Banking Organizations.”

In it, they cited “heightened risks associated with open, public, and/or decentralized networks.”

Since this time, we’ve seen the following:

On Jan. 9th, Metropolitan Commercial Bank announced a total shutdown of its crypto asset business.

On January 27th the Fed denies Custodia Banks’ 2-year application to become a member of the Federal Reserve system with a 100% backed crypto bank that would solve issues between crypto settlement (instant) and fiat settlement (not instant). This bank was specifically built to prevent bank runs, and the CEO is a 20-year Wall Street banking compliance veteran.

On January 27, the Fed also issues a policy statement, discouraging banks from holding crypto assets or issuing stablecoins, broadening their authority to cover non-FDIC-insured state-chartered banks.

On January 27, the National Economic Council shared a policy statement that strongly discouraged banks from transacting with crypto assets directly or maintaining exposure.

On February 9th, Kraken announced a $30 million settlement with the SEC over its Staking business and plans to discontinue the service.

On February 12, the SEC announced a lawsuit against a well-respected crypto infrastructure company, Paxos.

On February 23, Gary Gensler openly labeled every crypto asset other than Bitcoin as a security. [Does ‘ole Gary own some BTC?]

On March 9th, the NY Attorney General alleges ETH is a security

On March 20, the White House released its 2023 Economic Report. In it, they attempted to debunk just about every way that crypto solves actual real-world problems, without once addressing any of the problems from first principles.

On March 22, Coinbase announced that it received a Wells Notice from the SEC, despite Coinbase meeting with the SEC more than 30 times over the last 9 months. That’s almost once/week that Coinbase has been meeting with the SEC, sharing details of its business. Furthermore, the Coinbase S1 — a requirement to go public — had 57 references to its staking business (which appears to be in the crosshairs) as well as details on its asset listing process. The SEC approved all of this and now seems to be reversing course by regulating via enforcement action. This is quite shocking. Coinbase has vowed to fight, and the crypto community appears to be behind them.

Goodness, gracious.

My takeaway is that I’m happy to see bad actors brought to justice. We need a cleansing of the industry and we are getting it. And I want to see sensible regulation. We should absolutely regulate service providers so that retail is protected. But we need to leave the protocols alone so that innovation can blossom. Otherwise, the innovation will occur elsewhere, and the US loses. It’s that simple.

With that said, it appears that we are officially in the “and then they fight you stage.” Our government may be weaponizing access to the banking system, in an attempt to “shadow ban” legal businesses and the use of open-source technologies.

Quick side note: If you have crypto on any exchanges, it would be a good idea to withdraw to self-custody to be safe in our opinion.

Can access to Bitcoin or crypto be completely shut off? Highly unlikely. Just look at China and Africa to see how this goes. The people want crypto. This seems clear now. Therefore, a policy to “ban crypto” or enforce capital controls would likely backfire and make crypto assets more desirable.

In the event of a ban or shutdown of exchanges, I would expect to see rapid innovation that would attempt to circumnavigate any roadblocks put in place. The genie is out. We cannot put it back. But we should still expect attempts at stifling or slowing down the rate of adoption. It’s not supposed to be easy to disrupt major global markets.

Final Note on the Crackdown

Maybe I’m overreacting, but it seems like the US is being quite draconian here. It’s really too bad. It has a very “us vs them” vibe to it. It’s just really unfortunate because we really should be working together. At the end of the day, we’re talking about “open, public, and/or decentralized networks.” You’re reading this on an “open, public, and/or decentralized network. TCP/IP. HTTP. SMTP. VOIP. These are “open, public, and/or decentralized networks.” The government literally functions via an “open, public, and/or decentralized network.”

America was built on a foundation of property rights, rule of law, and freedom. From the first principles, shadow-banning open-source crypto networks would be akin to shadow-banning open-source internet protocols. A defensive, losing strategy. It feels very un-American. And it’s being driven by the fear of losing control. Which is sad. Because the idea of information and value flowing freely over “open, public, and/or decentralized networks” should absolutely be something that the United States embraces. And to be clear, open-source technologies are protected by the 1st Amendment as free speech. Which is likely why we see this softer, hidden approach.

One outcome here is that crypto could become a relevant topic during the 2024 elections. Crypto participants are bi-partisan, and actually lean more left. Most of these folks are from younger generations, which tend to be more Democrat. Yet Democrats in Congress seem to be where the draconian stance toward crypto comes from. I suspect many Democrats will be voting Republican in 2024.

Another outcome is that another region, such as the UK, takes the regulatory arbitrage play and captures this massive opportunity. In this case, companies such as Coinbase would simply relocate to a city such as London and have immediate connections with Singapore, Dubai, Europe, Australia, etc.

Finally, the truth will win out in the long run. I’ve found that as long as you stay focused on first principles, it is impossible to lose conviction in crypto. We’re on the right side of history. It’s that simple. That doesn’t mean it won’t be messy in the short run. I still think that most of the confusion with crypto will ultimately be remembered fondly in the years to come. We’ll have some good laughs about “JPM Coin,” private blockchains, and how everyone thought crypto was a scam.

If you’re interested in more on the “crypto crackdown,” I recommend Nic Carter’s work here, and here.

Looking Ahead

Banks aren’t lending. Commodity prices are dropping. ISM data is bleak. The 2-Year Treasury has become untethered to the Fed Funds rate. Markets are pricing in rate cuts by mid-year. Unemployment rates are likely to tick up.

This is deflationary, not inflationary.

My gut is telling me we are about to see a liquidity event. And it could be coming in the next few months. We’ll see how the next few weeks go regarding bank solvency. When this happens, we could see the Fed completely shift its monetary policy. A mountain of QE will be required to stabilize the system. Interest rates will drop. Bond prices will rise. The banks will stabilize.

As mentioned, this current crisis is induced by monetary policy. And it will be solved by monetary policy.

These conditions are likely to catalyze the next wave of growth in crypto, risk assets, and equities broadly.

Finally, I’ll leave you with this fascinating chart from Global Macro Investor showing the relationship between the Fed balance sheet and upcoming interest payments. Here is a tweet thread from Raoul Pal to go along with it. The bottom line is that QE is required for the United States (and EU, Japan, UK) to finance the outrageous debt levels.

The system simply cannot function without QE, and we have seen cycles of QE every 3.5 years since 2009. Why 3.5 years? Apparently this is the median debt maturity for public and private debt post-crisis when global interest rates were reset to zero. I found this particularly interesting because the Bitcoin Halving tends to line up with liquidity cycles (Bitcoin was released in January 2009). The end of 2023 and into 2024 & 2025 is the next debt refi period, and an even larger round of QE is required to fund it. When is the Bitcoin halving you ask? March of 2024.

Enjoy the ride. And stay safe out there.

Thanks for reading. As always, reply to this email if we can help with anything.

If you got some value from the report, please like the post, and share it with your friends, family, and co-workers so that more people can learn about DeFi and web3.

This small gesture means a lot and helps us grow the community.

If you have a comment, thought, or idea, drop it here:

Take a report.

And stay curious.

Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional and may hold positions in the assets covered. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general educational purposes only, is not individualized, and as such should not be construed as investment advice. The content contained in the report is derived from both publicly available information as well as proprietary data sources. All information presented and sources are believed to be reliable as of the date first published. Any opinions expressed in the report are based on the information cited herein as of the date of the publication. Although The DeFi Report and the author believe the information presented is substantially accurate in all material respects and does not omit to state material facts necessary to make the statements herein not misleading, all information and materials in the report are provided on an “as is” and “as available” basis, without warranty or condition of any kind either expressed or implied.

Gm Gm, Really loving this piece and the work you do here. I also run a web3 news substack for underrepresented creators called Facesofweb3. Would you be open to a recommendation exchange? Our subscribers need to be able to find each other!

Great job, once again!