Hello readers,

Deflationary. Yield Generating. ESG friendly. Is this a narrative Wall Street is about to embrace?

Many have speculated that Ethereum would one day “flip” Bitcoin and become the largest crypto network by market cap.

With Ethereum’s merge to Proof of Stake later this summer, ETH will check these three boxes: deflationary, yield generating, and ESG friendly. In this edition of The DeFi Report, we cover the upcoming changes to Ethereum’s monetary policy and what it could mean for investors.

Topics covered:

EIP1559 and changes to net new issuance of Ether

Post-merge monetary policy changes

Impacts on the liquid supply

The projected yield for staked ETH

Risks

Credit: Cointelegraph

*For what it’s worth, please note that I have not changed my thesis on Bitcoin, which I believe will capture Gold’s market cap sometime this decade. Those of you who have been reading along know that I do not get involved in the tribal nature of crypto. I simply try to analyze each network with clear eyes and develop a thesis as I see it. The fact that we still have a very tribal/contentious battle between supporters of Bitcoin and Ethereum tells me how early we still are. The market will eventually realize that pitting these two against each other is like comparing Apple to Netflix. Apples and oranges.*

Let’s go.

Ethereum’s Proof of Work Monetary Policy

Ethereum currently has a proof of work consensus mechanism (as does Bitcoin). Miners verify transactions on the network and receive 2 ETH/block + transaction fees and tips. The new issuance of ETH today amounts to an inflation rate of about 4.0%. This is the reward to miners for verifying transactions and securing the network. I like to think of blockchains as decentralized businesses - Ethereum is selling block space and the revenue goes to miners (soon to be stakers) all over the world who work for the network.

Source: Messari via Coinmetrics

EIP1559

Ethereum Improvement Proposal 1559 went live last August and introduced a change in compensation to miners for the transaction fees. Transaction fees come from ETH already in existence (already mined, so they are not part of new issuance). Below is a view of the transaction fees on the network over the last year - which were over $10 billion. Not too shabby.

Source: Token Terminal

The Ethereum Foundation determined that miners were overcompensated due to the high cost to transact on the network. Rather than excessively enrich miners, they determined that up to 70% of the transaction fees could be burned instead. This would offset the new issuance of ETH from each block of transactions and would drive more scarcity in the liquid float. These changes could influence the price and therefore compensate/incentivize all holders of ETH, rather than just the miners.

*Quick aside on the “burn” feature. This just means up to 70% of the fee paid is going to an address outside of anyone’s control. It is taken out of circulation. This is also happening with the dollar right now. When the Fed raises interest rates, there is less demand for loans. Less liquidity flows into the economy. Meanwhile, borrowers are still paying back their existing loans. The principal paid back is essentially “burned” as it is removed from the circulating supply. If more principal is paid back than money is lent out, we get less liquidity in the economy. This is the strategy to stifle inflation. We’ll see if it works. Furthermore, when the Fed pays down its balance sheet and stops buying treasuries (QE), we get more dollars being “burned” as they pay down their debt. This is tightening conditions, driving the dollar up, and causing broad sell-offs across assets. *

Since EIP1559 went into effect, about 13,467 ETH have been issued/day as new supply. This is the 2 ETH/block that is paid to miners. Meanwhile, 8,121 ETH have been burned/day on average - this comes from transaction fees (ETH that was already in the liquid float). This amounts to a 60% reduction in daily new supply since EIP1559 went into effect.

Source: Watch The Burn

When EIP1559 went live on 8/5/21, the price of ETH was $2,827. 3 months later ETH traded at $4,731, before selling off with the rest of crypto and equities broadly. Bitcoin was in a bull run during this time as well so it is difficult to quantify the impact that EIP1559 and the change to liquid supply had, but it likely played a role in the price action.

It’s worth noting that these changes are likely keeping ETH trading at a slightly elevated level in the bear market than we otherwise would see. Miners typically sell their coins back into the market to cover operating costs, so we’ve removed about 70% of the selling activity coming from transaction fee revenues. Using last year’s fee revenues, this would equate to a reduction of about $600k worth of selling activity/month.

Move to Proof of Stake

Ethereum is shifting its consensus mechanism to Proof of Stake this summer. Proof of Stake is a different system in which those who have staked their ETH will validate the transactions and receive the new issuance subsidy. The new system will use significantly less energy than Proof of Work and make the blockchain “ESG friendly.”

The key idea here is that validators will lock up their ETH as consideration to validate transactions. For doing so, they earn the block subsidy (+ transaction fees) going forward. Ethereum’s total supply today is 121 million ETH.

Source: Messari via Coinmetrics

Over the last year, approximately 5 million ETH entered the liquid supply as miners sold their newly minted coins. This selling pressure is likely to dissipate significantly as those staking ETH (replace the miners) don’t have any operating expenses to pay (electricity + GPU mining servers + hosting).

Monetary Policy Change

On top of all of this, the Ethereum Foundation is changing the monetary policy regarding the new issuance of ETH. Instead of rewarding 2 ETH/block to miners, the stakers/validators will receive rewards based on the total amount of ETH staked on the network.

Source: Ethereum Foundation

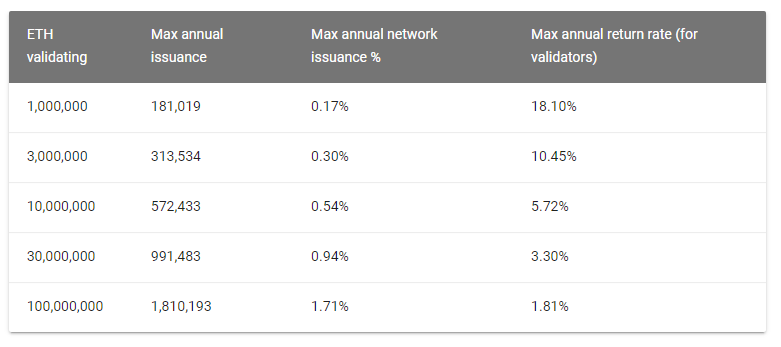

There is currently about 12.3 million ETH locked in staking contracts on ETH 2.0. This is about 9.6% of the total outstanding supply and would equate to an inflation rate of about .64%, compared to 4% pre-merge (see above).

The net-net here is that new issuance is dropping significantly. It looks like we’ll drop from about 5 million new coins last year to somewhere around 500k this year. On top of this, there will likely be less sell pressure since the rewards will go to stakers who have long-term convictions and no operating costs. And on top of that, we have 70% of the transaction fees being burned.

Here is a quick view of the simulation on UltraSound Money:

Based on the current projections, we will have a net new issuance of -2.5 million ETH over the next year. This equates to -2% inflation (deflation).

For these reasons, many are looking at this setup as a “three Bitcoin halvings” all at once.

Unlike Ethereum, Bitcoin has a very clear and predictable monetary policy that has never changed. Every 4 years new issuance is cut in half, hence the “halving.” For reference, below is a price chart showing the action each time the new supply issuance is cut in half. The red lines denote the date of the halvings and we can see the impact to price after each supply shock. Bitcoin’s inflation rate is currently 1.77%. This will move to .89% in May of 2024. It will drop in half every 4 years until all the Bitcoin has been mined (around the year 2140).

Will Ethereum see similar price action as a result of the supply shock to new issuance? Bitcoin bull runs typically take hold 3-6 months after the halving date.

Yield Generating Asset

The final takeaway from the merge to Proof of Stake is that ETH becomes a yield generating asset since validators will receive the subsidy and transaction fee rewards for locking up their coins. With about 12 million coins locked in staking contracts currently, it is projected that the yield to stakers will be about 5.3%. This is new issuance only. Let’s not forget that stakers will also receive the transaction fees and tips.

When we add in the tips and fees, it is likely the yield will be much closer to 10% and could be as high as 15% during bull markets due to network congestion (the move to PoS will not reduce transaction fees). As more validators come online, we should expect this figure to drop. Keep in mind that the yield here is earned in ETH. So, those with long-term convictions could potentially be sitting on quite the honey pot if Ethereum ultimately sees its potential over the next decade.

You might be asking: what happens if everyone staking their ETH exits their staking contracts? This is a great question. The answer is that staked ETH is a one-way street right now. Users will be locking their coins up for about 6 months post-merge until the Shanghai hard fork. Therefore, post-merge there will be zero new issuance entering the liquid supply for about 6 months. After this initial lock-up period, users will have to wait in a queue to exit their staked contracts which will likely take 2-3 weeks.

Risks

Unlike Bitcoin, everything about Ethereum is quite complex. The monetary policy changes. The blockchain leverages smart contracts and has a host of applications built on top of it that essentially trade like riskier derivatives of ETH today. All of the activity is speculative. Basically, Ethereum is flying much closer to the sun when compared to Bitcoin. For these reasons, there is significant risk in investing in ETH broadly, and certainly, risks related to this complex move to proof of stake. The Ethereum Foundation has planned this event for years and has been extremely thoughtful about its approach. Several testnets and simulations have been constructed in anticipation of the big event. Ancillary businesses have been working with the Ethereum Foundation for months and years in anticipation of the merge. With that said, things can go wrong. Investors should be clear-eyed about this.

The second risk is regulatory risk. We know it’s coming, and the fall-out from Terra could lead to more restrictive regulation. The market will likely overreact to this in the short run.

Furthermore, we are currently in a Fed tightening cycle from a macro perspective. It’s difficult to project how long this will go on, and how much pain the Fed will let the markets take. My guess is they will have to reverse course but if inflation persists, they may not. This would make it much more difficult for institutional money to flood into Ethereum. The best-case scenario would be to see the Fed reverse course around the same time that the merge is successfully completed.

My guess is that institutional capital is likely to wait to see how the merge goes from a technical perspective before deploying capital - this is the opportunity for retail to front-run the big boys. Of course, there is no reward without risk.

Conclusion

To summarize the changes:

Ethereum’s inflation rate is 4% today. This could shift to as low as -2.0% post-merge.

The change in new issuance of ETH post-merge amounts to 3 Bitcoin halvings all at once

The shift to proof of stake changes the dynamics for newly issued coins and liquid supply. Miners would typically sell their block subsidies to cover their operating costs. But stakers have no such operating costs. Therefore, we are likely to see significantly less sell pressure for the new issuance - which is likely to be about 1/10 of what it was pre-merge.

The already executed EIP1559 is burning about 70% of the transaction fees. The remaining fees will go to stakers post-merge.

The move to Proof of Stake will reduce Ethereum’s energy consumption by approximately 95%. Whether it is accurately placed or not, ESG is a narrative on Wall Street that matters right now.

Ethereum will become a yield-generating asset for validators/stakers. The anticipated yield post-merge is likely to be around 10% and could go even higher during periods when the network is congested.

Despite the bearish macro backdrop, the setup here for Ethereum over the next 6-12 months looks interesting for investors willing to stomach the risk.

As always, this is not investment advice. Please do your own research.

___

Thanks for reading and your continued support. If you got some value from this week’s report, please share it with your friends, family, and social networks.

If you have a question, comment, or thought, please leave it here:

Finally, if you would like to send me a tip, you can do so through the addresses below. If you do send a tip, please be sure to let me know so that I can send you a thank you note.

Bitcoin: bc1qghetd4g3lk7qnsn962amd9j92mkl4388zxz0jz

Ethereum: 0x084fcd3D9318bAa383B9a9D244bC0c32129EE20E

___

Take a report.

And stay curious my friends.

Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional and may hold positions in the assets discussed. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general investment information only, is not individualized, and as such does not constitute investment advice.