DeFi Financial Analysis

Metrics to track when analyzing lending/borrowing dApps

Hello readers,

I hope everyone had a nice weekend. This week we are covering an analysis of the more specific DeFi niche - lending & borrowing dApps (we’ll look at decentralized exchanges & insurance in a later post). With the recent correction in the broader market, the DeFi sector looks to have established a local bottom and currently represents only about 5% of the total crypto market cap.

In this report, we’ll examine some of the well-established DeFi lending/borrowing applications in the market, current valuations, and a thesis of where things could be heading.

If you are new to the program and would like to subscribe to have these free reports land in your inbox as they are published, drop your email below:

Let’s go.

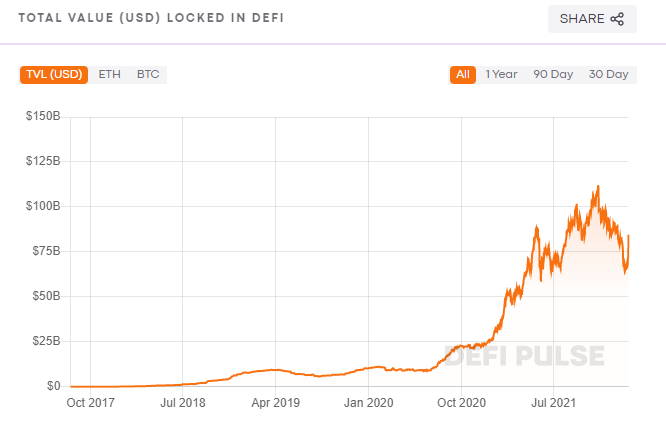

Total Value Locked

Source: DeFi Pulse

Total Value Locked in DeFi (Ethereum only) currently sits at about $85 billion, which is down from the peak of $110 billion back in November. Total Value Locked is measuring the total USD value of cryptoasssets that are staked in DeFi protocols. These are the assets that users are depositing into lending/borrowing pools as collateral for loans. We can think of this similarly to how we would think of the total deposits sitting at a bank. Those deposits are coming from customers like you and me, and the bank takes them and lends them out to 3rd parties, earning a spread on the interest they pay to you as the depositor, and the yield they get from the borrower on the other side.

Decentralized lending/borrowing is cool because it is performing the task of the bank without the bank sitting in the middle. Lenders can deposit collateral into lending pools, borrowers access that collateral for loans, and pay interest directly to the lender. There is no bank in the middle siphoning fees and taking a spread of the action. Instead, smart contracts perform the tasks which increase efficiencies, create a better user experience, and drive down costs. You know. Good tech doing what good tech does.

Lending/Borrowing dApps

Let’s take a look at Aave - one of the larger and more established lending and borrowing applications in the DeFi space.

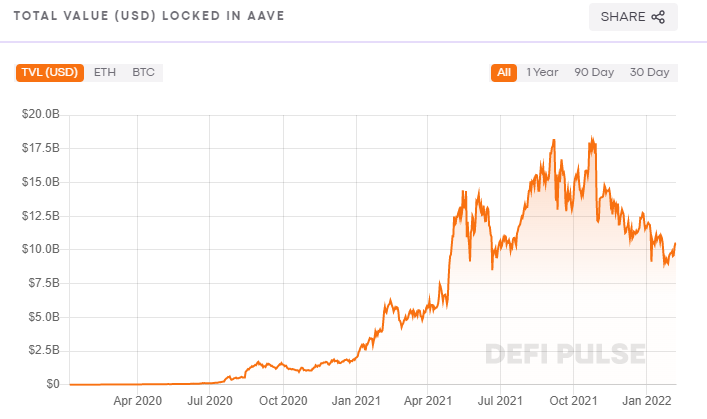

Aave

Source: DeFi Pulse

Total Value Locked in Aave currently sits at about $10 billion, down from the peak in November of $18 billion.

What does this mean for user revenues (interest paid to depositors/lenders)?

Source: Token Terminal

If we take out the brief spike back in November, revenues were peaking out around $2 million per day when TVL was also peaking. Today, revenues are averaging about $600-$700k. So, TVL dropped about 45% from the peak. Meanwhile, revenues dropped more than that, about 65%. These are rough figures but they give us a sense of how these applications function. As $ flows in and out, so too does the revenues that users are earning on the protocol. And if demand leaves first, rates drop, and revenues decrease.

But how did this influence the price of the Aave token?

Source: Coinmarketcap

The price of the Aave token is down 54% from the highs in November, and down 76% from the all-time highs. Total Value Locked tends to lead the movement in revenue, which then impacts the price of the coin. Below is a comparison of Aave, Compound, and MakerDAO - the 3 largest DeFi lending/borrowing applications.

By analyzing these metrics across various periods, we can begin to get a sense of when the market is under or overvaluing different protocols. As we can see, Maker has held up favorably in terms of TVL. The price is down about 63%, but revenues are down about 50%. This has led to a favorable drop in Price to Sales - making the protocol look relatively undervalued today. *Interestingly, with TVL holding up well (15% drop), revenues still dropped off almost 50%. This means that interest rates dropped significantly. This makes a lot of sense - there was a ton of collateral still in the protocol but demand vanished. The result is a drop in interest rates since these markets are truly free and based on supply/demand (and not the Federal Reserve).

Meanwhile, the price of Aave is down 76% from its high. Again, revenues have not dropped in line with the drop in market price. As such, the Price/Sales ratio is down only 62%. This points to the protocol looking relatively undervalued at the current market price.

If we look at Compound, the market price is currently 84% off its all-time high. But revenues have not dropped in line with the drop in market price - again, it appears the market overshot the correction here. We can observe this by tracking the drop in Price/Sales relative to the drop in market price. Revenues have not dropped off the same cliff, therefore the Price/Sales ratio is down only 65%. When price/sales do not drop in line with price, we know that revenues have held up better than the token price.

Finally, in case you were curious, below are some stocks to compare to. In my view, the P/E ratio is the one we should be looking at when comparing to a traditional company. P/E is measuring the actual payments made to shareholders which is equivalent to P/S for crypto protocols. With crypto lending/borrowing protocols, sales are distributed directly to the users - essentially the same ways earnings are distributed to shareholders. Albeit, this happens quarterly for traditional companies while crypto protocols are constantly paying out the earnings in real-time.

It’s interesting to see Coinbase, the only crypto company included (and the only company in hyper-growth mode), as the cheapest-looking company out of the bunch when compared to other large tech companies.

Conclusion

Crypto markets run on fear and greed. The best way to track this is by looking at the data. I find that the best metric to track for the lending/borrowing applications is Price/Sales. It gives us a great marker for analyzing when the market price is separating from the revenues of the protocol. During price peaks, we see Price/Sales shoot up. And during market corrections we see it drop. When we see market price rise or drop significantly greater than the move in revenue, we know that the market is not acting rationally. These are the best times to be buying or selling these assets.

It is my sense that broadly speaking, the DeFi niche of crypto (lending/borrowing, decentralized exchanges, and insurance) is likely the most undervalued sector of the market today. We saw NFTs and the Metaverse capture the hearts and minds of folks throughout 2021. DeFi took a back seat. However, DeFi has been around longer, has a more established tracked record, is producing real revenue, and the builders of these protocols keep improving them. For example, Aave recently released Aave Arc (permissioned DeFi), with Fireblocks (recent $8b valuation) taking the lead as the first institutional player to integrate with them. It won’t be long before Compound moves in this direction as well. MakerDAO is leading the charge with bringing real-world assets into DeFi. These protocols are at the base of an emerging new financial system, getting stronger and stronger, yet the market seems to be asleep at the wheel in my opinion. Finally, the DeFi niche represents roughly 5% of the total crypto market today. This is likely WAY too low. The total addressable market for DeFi is massive. We should expect DeFi to garner closer to 40-50% of the market as these protocols mature, as institutions come in (permissioned DeFi), and as the market moves off the NFT high.

Finally, we are now seeing some interesting DeFi activity on Layer 2 (with even lower P/S ratios). We’ll be covering this in more detail in a future post.

Please note that I am not a financial advisor and this information is for educational purposes only. I just enjoy studying this stuff and sharing it with you.

___

Thanks for reading and for your continued support. If you have a question, comment, or thought, leave it here:

I hope you got some value from this week’s report. If you did, please share it with your friends, family, and social networks so that more people can learn about crypto and this exciting new innovation.

Finally, if you would like to send me a tip, you can do so through the addresses below. If you do send a tip, please be sure to let me know so that I can send you a thank you note.

Bitcoin: bc1qghetd4g3lk7qnsn962amd9j92mkl4388zxz0jz

Ethereum: 0x084fcd3D9318bAa383B9a9D244bC0c32129EE20E

___

Take a report.

And stay curious my friends.

Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general investment information only, is not individualized, and as such does not constitute investment advice.