Central Bank Digital Currencies

CBDCs are coming. How will they impact crypto?

Hello readers,

I’ve been thinking a lot about two big developments in the Web3 space over the past month:

Paypal launched a stablecoin on Ethereum

Worldcoin launched a solution to tie human identity to digital wallets via biometrics on Ethereum

As always, we’re laser-focused on what this could mean in the big picture. Central Bank Digital Currencies (CBDCs) were the first to come to mind. In this week’s report, I’m sharing a deep dive into CBDCs in an effort to forecast their impact on crypto and *public* blockchains. Topics covered:

Current Progress amongst the Major Economies

Why CBDC? What are the Proposed Benefits?

What are the Tangential Impacts?

Implementation: Public vs Private Blockchains

What do CBDCs mean for Bitcoin and Ethereum?

Disclaimer: Views expressed are the author's personal views and should not be taken as investment or legal advice.

If you find our free research & analysis helpful, please like the post — which can be done directly from your inbox via the heart button in the upper left. Let’s make quality free content a win/win. This helps grow the community and responsibly introduce more people to DeFi and Web3.

The Ethereum Investment Framework is still 50% off. I’m excited to share that Glassnode is sponsoring our Q3 update, but the price is also increasing. You can lock in quarterly updates here at just $27.72/issue: The Ethereum Investment Framework

The DeFi Report newsletter is a data-driven exploration of the Web3 tech stack from first principles & on-chain data.

Let’s go.

Status of CBDC Progress

Below is a global map of CBDC projects courtesy of the Atlantic Council. It reveals the following:

A total of 130 CBDC projects

11 Launched (pink)

21 in Pilot mode (green)

33 in Development (teal)

47 at the Research stage (blue)

16 inactive (gold)

2 canceled (red)

130 countries representing 98% of the world’s GDP are currently working on a CBDC. This figure is up from just 35 countries three years ago. Furthermore, the number of wholesale CBDCs (cross-border transactions between governments & institutions) has doubled since Russia was shut out of the international SWIFT system after invading Ukraine.

Major Economies

China: The digital yuan is currently the furthest along, though it says more about their competition than actual progress on China’s part. After nearly 10 years of development, the “pilot program” is live and has seen $249b in transactions while integrating with about .16% of the money supply. Some believe China is calling it a “Pilot” simply because the program hasn’t taken off.

While the government struggles to find traction with its CBDC within Chinese borders, it continues to look elsewhere. For China, there is a geopolitical upside in creating an alternative payment rail that the US does not control. The “exorbitant privilege” bestowed on the US via the dollar hegemony could be undermined if currencies like the Chinese yuan become more prevalent in global trade. Therefore, finding trading partners for the digital yuan is a priority, though progress is slow.

The implementation of the digital yuan was done through a non-blockchain distributed ledger with the banks providing intermediary services between the People’s Bank of China and Chinese citizens and businesses.

Japan: The Japanese Yen recently commenced its Pilot program, in which 60 of the country’s largest businesses are participating in simulated transactions. The program comes on the heels of 2 years of experiments using both traditional and private/permissioned DLT databases. Similar to China, Japan would issue its CBDC to commercial bank intermediaries rather than directly to citizens & businesses. *Interoperability was cited as a key concern during testing. We’ll come back to this later.

Brazil: Recently delayed the commencement of its Pilot program for its CBDC, named “DREX.” Brazil is using Hyperledger Besu — a private/permissioned DLT that is based on the Ethereum Virtual Machine. The source code has been open-sourced on Github. Privacy concerns have been the biggest hurdle so far.

United States: The US is currently in the development stage. Project Hamilton, a joint effort between the Boston Fed and MIT was completed at the end of 2022. It included a two-phase approach in which a permissioned blockchain was tested in Phase 1. The code was open-sourced for the project — which saw a peak performance of 170k transactions/second. Phase II used a non-blockchain solution in which the throughput resulted in a higher 1.8m transactions/second. There is no identity solution today, but the project summary indicated it could be added in the future. The implementation would include intermediaries such as commercial banks sitting between the Central Bank and businesses/individuals.

A separate initiative by the NY Fed (Project Cedar) recently completed its Phase 2 testing for a “wholesale” CBDC alongside the Monetary Authority of Singapore. The project aims to create a network of permissioned chains that are interoperable, with each Central Bank controlling its own chain. The goal is to reduce settlement times, remove intermediaries, run 24/7, and centralize common processes.

There were two primary “cons” cited in the report that stuck out to us:

“Establishing multi-party governance structure for a common network while maintaining independence is non-trivial.”

“Requires agreement and alignment to common technical stack and standards.”

There’s some signal here. We’ll circle back to this later in the report.

Europe: Europe is still in its “investigation phase” as it pertains to CBDCs. The ECB recently published its 3rd progress report on the matter. Per the report, we should expect an update covering the “high-level comprehensive design” of the CBDC sometime later this year. A decision on the type of technology to use (DLT or other) has not been made at this time. There’s not much to add on this one. It feels like Europe and the ECB are behind the others, though nobody really has anything figured out just yet.

A Few High-Level Takeaways:

I spent 10+ hours reading through published materials and reports on each jurisdiction’s research, design choices, testing, etc.

It’s appears that none of them have anything figured out right now.

When you read the CBDC reports being put out by each Central Bank (I’ll link to a bunch of them at the end of the report) you get the vibe that “someone’s boss told them to do something.” The people tasked with these initiatives might be in over their heads. Remember, the government is just people. They’re fumbling around. Trying some stuff. Sharing their findings. And making some progress here and there.

Why CBDC? What are the Proposed Benefits?

In each jurisdiction, the proposed benefits are touted as follows:

Faster settlement

Cross border payments

Lower costs

24/7, 365

Democratize access to financial services

Ability to stimulate the economy (Covid was a catalyst here)

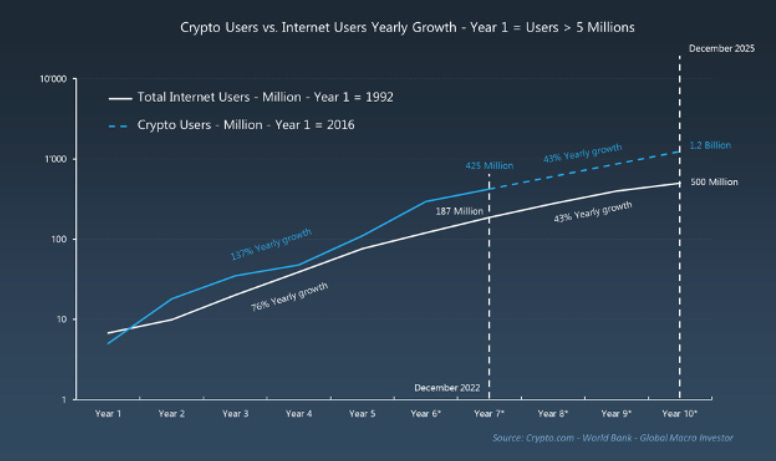

This is all fair. But what you don’t hear about is the fact that crypto has 300+ million users globally (crypto.com puts the number at 425 million). More than 10% of people in the US, Europe, the UK, UAE, and Australia own or have owned crypto. Hundreds of millions of crypto users reside in China, Japan, and India.

Globally, crypto continues to grow at a faster pace than the Internet:

Source: crypto.com, world bank, global macro investor

Payment providers and Fintechs such as Visa, Mastercard, Paypal, Stripe, etc. are integrating with *public blockchains* (crypto) to drive mainstream adoption.

The Ethereum public network itself has over 100 million non-zero wallets. Bitcoin has over 45 million.

CBDCs are a technological upgrade. But they’re also a response to crypto, and an attempt to hold onto government-issued currency. You’ll never hear that come from a Central Bank or anyone pushing a CBDC. And that’s ok. We shouldn’t expect the gov’t to just give up its monopoly on money.

With that said, it’s a bit awkward for the government to be competing with the private market in terms of technological development. The government is good at creating rules and regulations. The private sector typically handles innovation. There is a good reason for this: incentives. A government worker cannot become rich and famous by working on a CBDC project. But an entrepreneur can. Therefore, the entrepreneur works nights and weekends. The gov’t employee punches in at 9am and punches out at 5pm.

For this reason, we think the infrastructure for CBDCs will be created by the private sector — which we get to later in the report.

Potential Impacts

We think it’s fair to say that we’re entering a period of currency wars.

If you’re reading this, that’s probably not news to you.

Of course, the dollar isn’t going away anytime soon. But history says that money has always changed. As do reserve currencies. Therefore, the dollar has probably seen its heyday.

Crypto and the launch of CBDCs worldwide are bringing this to the forefront. A cascade of tangential implications could surface as a result:

The General Public & Money

Before the printing press was invented, I doubt lots of people were thinking about the implications of the Church and State being tied together at the hip.

The Printing Press played a role in bringing this to the forefront. It got people thinking. It elevated the consciousness of society. Things eventually changed.

We believe Bitcoin is doing this today. Gradually…then suddenly as they say.

We expect the debate around CBDCs to create heightened awareness as well. This leads to my next point…

CBDCs are Becoming Political

We’ve already seen politicians come out and attempt to ban CBDCs in the US. The Republic Presidential Debates kicked off a few weeks ago. Crypto and CBDCs have not come up yet. But we expect this to become a hot-button issue at some point during the election cycle.

What happens when more people start to think about CBDCs? About money? About the state’s control over money? Remember, trust in Government (and institutions broadly) is near all-time lows in America, where it’s been for a decade now.

What will people think about Bitcoin as they learn more about money and the fact that the government now wants to issue its own “crypto token?” In this regard, CBDCs could become a global advertising campaign for Bitcoin.

The Dollar and International Trade

The dollar could lose its importance in international trade if other countries launch CBCDs first, price their commodities in those currencies, and start trading with each other in those currencies. Currency wars typically lead to hot wars. I hate to say that. But it is a historical precedent. Maybe this time we get “cyber wars.” Who knows. Some would argue it’s already happening today.

What does a CBDC mean for Banks?

It’s possible that a CBDC would restructure the banking system. If every citizen has an account with the Fed, do we need commercial banks anymore? Or are we just going to re-create the current monetary system on better rails?

Privacy & Control

If the government controls the ledger and the ability to mint currency, it could theoretically control the economy with more precision. It’s possible that funding could be directed to politically favored initiatives and businesses — while shutting off funding for others. Funds could arbitrarily be frozen — for example to stifle protests (as we saw in Canada last year).

Government-issued currency on a blockchain will undoubtedly lead to more control if the right protections are not put into place.

CBDCs and Public vs Private/Permissioned Blockchains

If you’re reading The DeFi Report, you probably know that we think “permissioned blockchains” are a bit of a misnomer.

Not surprisingly, some CBDC projects we’ve looked at are being tested on private/permissioned chains. Others don’t even use blockchain in any form — often referred to as some type of “distributed ledger technology.”

We think that Private/permissioned blockchains will not work for CBDCs. There are several reasons for this.

Interoperability & Shared Standards

The NY Fed testing revealed that “establishing a multi-party governance structure for a common network while maintaining independence is non-trivial.”

We think it’s more than just “non-trivial.” It just flat-out doesn’t work. We know this because it’s been tested several times via “blockchain consortiums.”

The bottom line is that nobody wants to join someone else’s network — giving away data and control in the process. It turns out that for every “blockchain consortium created,” two more private networks were created (per a Forrester study commissioned by E&Y).

If it doesn’t work for financial institutions, it certainly won’t work for sovereign Governments.

The NY Fed tested a private consortium network where each Central Bank runs its own chain (Project Cedar). This solves the privacy/data issue. But it introduces an interoperability/technical challenge…

“requires agreement and alignment to common technical stack and standards.”

Does anyone think we’re going to get a bunch of governments around the world to coordinate to build on the same tech stack, where nobody owns or controls it??

Hey guys. This already exists. They’re called *public blockchains.* They’re decentralized — so that you don’t have to trust that some other entity won’t kick you out of the network or steal your data. Ethereum is the largest one today. It already has shared standards around token design, programming languages, wallets, identity, etc.

We’ve already solved the interoperability challenge. Furthermore, public blockchains have more security, massive network effects, and a global hive mind of brain power working on them.

You don’t have to build all of these things yourself.

Oh, and by the way — you can have your own “private network” as an L2 on Ethereum. You can then opt into a set of shared standards. You’ll be interoperable with other governments and connected to 8 billion people.

Within your own L2, you can mint currency. You can interact with intermediaries (banks). You can track everything on a transparent ledger while maintaining privacy with zero-knowledge proofs. This means you can “prove” monetary policy to the general public without revealing the details of everyone’s private data. You’ll be able to track everything to ensure tax receipts are collected. Law enforcement will be able to use the blockchain to trace money laundering. Regulators will have more transparency into systemic risks.

This can all be set up with a proper rule-set for what is acceptable and what is not — as determined by the voters. For example, the government should be able to use the ledger to hunt down criminal activity and tax fraud. But they shouldn’t be able to arbitrarily spy on its citizens and censor user behavior (4th Amendment).

Privacy, Control, and Identity

Most crypto users don’t realize this, but Tether can freeze and seize your assets. So can USDC and PayPal. Of course, they can also mint assets.

Governments will have the same control — on *public blockchains.*

Regarding identity, this hasn’t been solved (or seemingly considered) with CBDC testing. Worldcoin is the first reputable project we’ve seen with a viable solution that ties human identity to public blockchain wallets via biometrics. Is Worldcoin the final solution here? Time will tell. But this is another missing piece available on *public* blockchains that governments haven’t quite figured out.

Ethereum

We believe CBDCs will ultimately be issued on *public* blockchains. The most obvious choice would be Ethereum. Of course, scalability and privacy are the key missing ingredients today. These constraints are being solved by increased throughput on L2s + zero-knowledge proofs. We are nowhere near being able to support the global economy today. But Moores's Law is at play. People forget that the internet couldn’t support Zoom, YouTube, and Games until recently. Moore’s Law is playing out slowly.

But it’s playing out. We’re seeing this in real time on Ethereum. All you have to do is look at the transaction activity on L2s today. It’s already surpassing that of Ethereum at the L1. Consider that L2s had about 1/100th of Ethereum’s volume just 2 years ago.

Data: Orbiter Finance

We can see Moore’s Law playing out in the transaction/second (throughput) data as well:

Data: L2beat

Naturally, we’re seeing more and more value locked on L2s:

Data: L2beat

We see lots of folks making the mistake of assuming that “Ethereum isn’t scalable.” This view ignores the power of network effects and Moore’s Law.

Bitcoin

As we get closer to the implementation of CBDCs (many years away), we think this is going to make Bitcoin’s value proposition more obvious.

Bitcoin is simple. It doesn’t do much. It just ensures that there is only so much of it. And if enough people think that scarcity + decentralization is valuable, it’s valuable. The output of people thinking it’s valuable is that they will hold the asset. Eventually, they’ll be willing to exchange goods and services for it. It’s really that simple.

Bitcoin is a better version of gold because it is justifiably scarce and it comes with a global, peer-to-peer payment network. That’s it.

We think that CBDCs will ultimately be built on Ethereum as L2s (or possibly another public network).

But their existence (and the heightened public consciousness about money) could drive Bitcoin adoption as well.

Conclusion

CBDCs are coming.

With that said, they are many years out. Watching Central Banks fumble through testing and research on CBDCs is reminiscent of enterprises doing the same thing on private/permissioned blockchains in 2018/2019.

We think they’ll continue to research and test for several years to come. Meanwhile, Ethereum and other public networks will continue to scale and grow. Moore’s Law will continue to play out. Scalability and privacy will continue to develop on Ethereum.

Eventually, Central Banks will come around to public blockchains. They’ll realize they can have their own blockchain — connected to a global, credibly neutral, open standard that doesn’t require each party to trust the other.

How much is the winning settlement network worth at that point?

Thanks for reading.

If you got some value from the report, please like the post, and share it with your friends, family, and co-workers so that more people can learn about DeFi and Web3.

This small gesture means a lot and helps us grow the community.

Finally, if you have a comment, thought, or idea, drop it here:

Take a report.

And stay curious.

Resources

Atlantic Council CBDC Tracker: https://www.atlanticcouncil.org/cbdctracker/

Chainalysis Coverage on CBDCs: https://www.chainalysis.com/blog/central-bank-digital-currencies-cbdc/

McKinsey Report: https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-central-bank-digital-currency-cbdc

US Project Hamilton: https://www.bostonfed.org/news-and-events/news/2022/12/project-hamilton-boston-fed-mit-complete-central-bank-digital-currency-cbdc-project.aspx

US Project Cedar: https://www.newyorkfed.org/aboutthefed/nyic/project-cedar

Europe: https://www.ecb.europa.eu/press/pr/date/2023/html/ecb.pr230424_1~395626f0d9.en.html

Japan: https://kilpatricktownsend.com/en/Blog/Digital-Assets-Regulation/2023/6/Japan-Central-Bank-Digital-Currency-CBDC-Bank-of-Japan-Completes-Proof-of-Concept

https://www.boj.or.jp/en/paym/digital/index.htm

China: https://www.fpri.org/article/2023/06/china-is-doubling-down-on-its-digital-currency/

https://www.technologyreview.com/2023/08/03/1077181/whats-next-for-chinas-digital-currency/

Brazil: https://www.coindesk.com/policy/2023/05/25/brazils-central-bank-selects-14-participants-for-cbdc-pilot/

https://github.com/bacen/pilotord-kit-onboarding

https://www.reuters.com/markets/currencies/privacy-market-maturity-hurdles-facing-brazils-cbdc-rollout-cenbank-official-2023-08-29/

Disclaimer: Individuals have unique circumstances, goals, and risk tolerances, so you should consult a certified investment professional and/or do your own diligence before making investment decisions. The author is not an investment professional and may hold positions in the assets covered. Certified professionals can provide individualized investment advice tailored to your unique situation. This research report is for general educational purposes only, is not individualized, and as such should not be construed as investment advice. The content contained in the report is derived from both publicly available information as well as proprietary data sources. All information presented and sources are believed to be reliable as of the date first published. Any opinions expressed in the report are based on the information cited herein as of the date of the publication. Although The DeFi Report and the author believe the information presented is substantially accurate in all material respects and does not omit to state material facts necessary to make the statements herein not misleading, all information and materials in the report are provided on an “as is” and “as available” basis, without warranty or condition of any kind either expressed or implied.